+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global Liquid Chemical Seaborne Logistics Market to Reach $24.46 Billion by 2031, Growing at 2.0% CAGR

Global Liquid Chemical Seaborne Logistics Market to Reach $24.46 Billion by 2031, Growing at 2.0% CAGR

Thursday,02 Jul,2026

Liquid Chemical Seaborne Logistics: Definition and Principles

Liquid chemical seaborne logistics involves the specialized transportation of liquid chemicals via ships, adhering to strict safety, environmental, and regulatory standards. This sector requires specialized tankers (chemical tankers) and handling procedures due to the diverse and potentially hazardous nature of the chemicals being transported — ranging from bulk commodity chemicals (sulfuric acid, caustic soda, methanol, ethylene glycol) to high-value specialty chemicals (ultra-pure electronic-grade liquids, pharmaceutical intermediates, agrochemicals).G$M~}8F7S_~9.webp)

Key characteristics of the market:

-

High specialization: Chemical tankers are not one-size-fits-all. Vessels are designed with dedicated cargo tanks (stainless steel, coated mild steel, or fully lined) and segregated pumping systems to prevent cross-contamination between different chemical grades.

-

Stringent regulatory compliance: The International Maritime Organization's (IMO) International Code for the Construction and Equipment of Ships Carrying Dangerous Chemicals in Bulk (IBC Code) governs vessel design, construction, equipment, and operations. Compliance with REACH (EU), TSCA (US), and other regional regulations adds layers of documentation and operational requirements.

-

Diverse cargo types: Organic chemicals (solvents, intermediates, acids, esters, glycols, alcohols), inorganic chemicals (sulfuric acid, phosphoric acid, caustic soda, chlorine derivatives), specialty chemicals (surfactants, monomers, electronic chemicals), and green/bio-based chemicals (organic acids, hydrogen peroxide, bio-alcohols).

-

Infrastructure: Requires specialized ports and terminals with dedicated berths, stainless steel or coated pipelines, vapor recovery systems, and spill containment facilities.

-

Trade route dynamics: Driven by regional production imbalances: China dominates inorganic chemicals production (sulfuric acid, phosphates, caustic soda); Europe and North America lead in high-value organic chemicals (specialty solvents, intermediates); Middle East and North America are major producers of petrochemical feedstocks (methanol, ethylene glycol, para-xylene).

Liquid Chemical Seaborne Logistics Market Summary

According to a new market research report published by Market Monitor Global, the global Liquid Chemical Seaborne Logistics market is projected to reach USD 24.46 billion by 2031, at a compound annual growth rate (CAGR) of 2.0% during the forecast period. This modest but steady growth is driven by robust demand from key end-use industries (pharmaceuticals, agrochemicals, specialty chemicals, and petrochemicals), regional production imbalances that sustain long-distance trade flows, and ongoing investments in specialized chemical shipping infrastructure.

Market Monitor Global's analysis indicates that the global key manufacturers of Liquid Chemical Seaborne Logistics include Stolt-Nielsen (UK), Odfjell (Norway), MOL Chemical Tankers (Japan), Inner Mongolia Junzheng Energy and Chemical (China), Iino Kaiun Kaisha (Japan), Hansa Tankers (Norway), Team Tankers (Switzerland), MTMM (South Korea), Bahri (Saudi Arabia), and WOMAR (Japan/Singapore). In 2024, the global top 10 players collectively accounted for approximately 71.0% of total revenue, indicating a moderately concentrated market with a few large, established chemical tanker operators dominating the segment, alongside many smaller regional players and specialized niche operators.

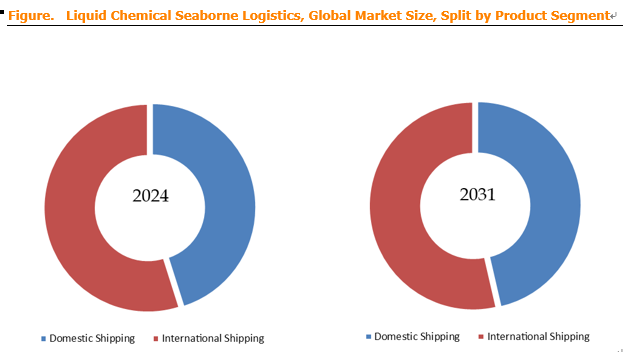

In terms of product type (by service category), International Shipping is the largest segment, holding a 54.9% share. This includes deep-sea, cross-ocean voyages (e.g., US-Gulf to Asia, Middle East to Europe, Asia to Americas) that move large volumes of liquid chemicals between major production and consumption regions. Coastal/Regional Shipping and Inland Waterways account for the remainder, serving domestic or short-sea routes (e.g., intra-Asia, intra-Europe, US Gulf coast to East coast).

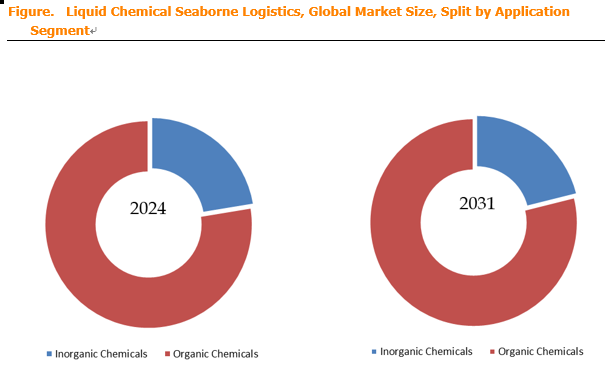

Regarding application (by cargo type), Organic Chemicals is the largest segment, accounting for 77.6% of the market. Organic chemicals include a vast range of products: solvents (acetone, toluene, xylene), alcohols (methanol, ethanol, isopropanol, ethylene glycol), glycol ethers, esters (ethyl acetate, butyl acetate), monomers (styrene, vinyl acetate), acids (acetic acid, acrylic acid), and surfactants. Inorganic Chemicals (sulfuric acid, phosphoric acid, caustic soda, sodium hydroxide, chlorine derivatives) account for the remainder. The organic chemicals segment is larger due to the sheer diversity of products, higher volumes traded globally, and the higher value and specialty nature of many organic liquid chemicals.

Regional dynamics: Asia-Pacific is the largest and fastest-growing consumer region, driven by China's massive domestic chemical industry (both production and consumption), rapid industrialization in India and Southeast Asia, and the region's role as a manufacturing hub. North America (particularly the US Gulf Coast) is a major production region for organic intermediates and petrochemicals, with significant export volumes. Europe is a high-value market, importing organic intermediates and speciality chemicals while exporting its own high-value products (pharmaceutical intermediates, agrochemicals). The Middle East (GCC countries) is a major producer of petrochemical feedstocks, particularly methanol, ethylene glycol, and para-xylene, with exports to Asia and Europe.

I_0I1HZ(8177}{59J32.png)

Liquid Chemical Seaborne Logistics Market Dynamics

Market Drivers:

-

D1: Robust demand from key downstream industries – The end-use industries driving chemical demand are expanding steadily: the global pharmaceutical market (projected to exceed $2 trillion by 2030), the agrochemical market (growing with global population and food demand), and specialty chemicals (adhesives, coatings, electronic chemicals, personal care, detergents). Each of these industries relies on liquid chemical feedstocks that must be transported internationally by specialized tankers.

-

D2: Regional production imbalances driving trade flows – Global chemical production is highly concentrated:

-

China dominates inorganic chemicals (over 50% of global sulfuric acid, phosphates, and caustic soda capacity) and is a major producer of organic chemicals (methanol, ethylene glycol, acetic acid).

-

Europe is a leader in high-value organic chemicals (pharmaceutical intermediates, solvents, speciality surfactants).

-

North America (US Gulf) is a major petrochemical production hub (ethylene, propylene, methanol, ethylene glycol).

-

Middle East exports large volumes of petrochemical feedstocks (methanol, ethylene glycol, para-xylene) to Asia.

These production-consumption imbalances sustain long-distance seaborne trade routes, driving demand for chemical shipping services.

-

-

D3: Stricter environmental and safety regulations – IMO’s chemical tanker standards (IBC Code), MARPOL Annex II (regulations for the discharge of noxious liquid substances), and regional regulations (REACH, TSCA, China's GB standards) require operators to invest in advanced stainless steel and epoxy-coated vessels to ensure cargo purity and prevent contamination. The capital expenditure required for modern chemical tankers (stainless steel tanks, double-hull designs, sophisticated cargo handling systems) is substantial but essential for regulatory compliance and customer trust.

-

D4: Growing adoption of green and bio-based chemicals – The transition toward sustainable chemistry is opening new shipping opportunities:

-

Bio-based organic acids (lactic acid, citric acid, gluconic acid) — used in bioplastics, food, cosmetics.

-

Bio-alcohols (bio-ethanol, bio-butanol) — used as fuels, solvents, and chemical feedstocks.

-

Hydrogen peroxide solutions — used for green bleaching, water treatment, and increasingly in chemical synthesis.

-

Other bio-based chemicals (succinic acid, 1,3-propanediol, bio-based solvents).

These chemicals often have specific handling requirements (temperature control, inerting, purity) that require specialized tanker services, creating niche growth opportunities.

-

-

D5: Supply chain diversification and nearshoring trends – The COVID-19 pandemic and geopolitical tensions (US-China trade friction, Europe-Russia energy dependencies) have accelerated supply chain diversification. Chemical buyers are seeking to reduce dependence on single-source regions, increasing the complexity of logistics and requiring more flexible, responsive shipping solutions. This diversification benefits the seaborne logistics sector by increasing the number of trade routes and ports served.

NRB~TLF1P.png)

Market Restraints:

-

R1: High capital intensity and operating costs – Chemical tankers are among the most expensive vessels to build and operate. Stainless steel tankers (required for many high-purity and high-value chemical cargoes) cost significantly more than coated mild steel tankers. Operating costs are also higher: specialized crew training, IBC Code compliance, cargo handling equipment, environmental protection systems (scrubbers, ballast water treatment), and insurance premiums all add to costs. The high capital expenditure and operating costs limit entry to well-capitalized players and create barriers for smaller operators.

-

R2: Regulatory complexity and compliance burden – Chemical shipping is subject to a complex web of international, regional, and national regulations:

-

IMO's IBC Code and MARPOL Annex II.

-

European REACH and CLP (Classification, Labeling and Packaging) regulations.

-

US TSCA and EPA regulations.

-

China's GB/T standards and environmental regulations.

-

Port state control inspections.

-

Cargo declaration, safety data sheet (SDS) management, and emergency response plans.

Compliance requires significant administrative resources, legal expertise, and ongoing training. Non-compliance can result in fines, detention, or even vessel seizure. This regulatory burden increases operational costs and deters new entrants.

-

-

R3: Volatility in freight rates and shipping demand – The chemical shipping market is influenced by macroeconomic cycles (GDP growth, industrial production), chemical demand fluctuations, vessel supply, and energy prices (affecting fuel costs). Freight rates can be highly volatile, making revenue forecasting difficult for operators. In periods of oversupply, rates may fall below operating costs; in periods of high demand and tight vessel supply, rates can spike.

-

R4: Environmental pressure on the shipping industry – The shipping industry faces increasing environmental scrutiny, including:

-

IMO's 2020 Global Sulphur Cap (limiting sulfur content in marine fuels to 0.5%).

-

IMO's 2023 GHG Strategy (targeting net-zero emissions by 2050).

-

EU Emissions Trading System (ETS) inclusion of shipping.

-

Regional carbon taxes and port emissions fees.

Compliance requires investment in low-emission fuels (LNG, methanol, ammonia), energy-efficient technologies, and potentially carbon capture systems. For chemical tanker operators, these investments add to capital and operating costs, pressuring margins.

-

-

R5: Geopolitical uncertainties and trade frictions – The chemical shipping market is affected by geopolitical events:

-

US-China trade disputes have led to tariffs on chemical products, altering trade flows.

-

Russia-Ukraine conflict has disrupted chemical supply chains (Russia and Ukraine are significant producers of ammonia, fertilizers, and petrochemicals) and increased energy prices.

-

Red Sea shipping route disruptions (Houthi attacks on shipping in the Red Sea) have rerouted vessels around Africa, increasing voyage times and costs.

-

Drought conditions in the Panama Canal have limited transits, affecting route choices.

These uncertainties increase operational complexity and costs for chemical tanker operators.

-

Market Opportunities:

-

O1: Specialized fleet segmentation and high-margin niche chemicals – Parcel tankers are increasingly catering to high-margin niche chemicals: ultra-pure electronic-grade liquids (used in semiconductor manufacturing, requiring extreme purity — up to 99.999999% purity; special handling to prevent contamination), pharmaceutical intermediates (temperature-sensitive, requiring dedicated tankers with heating/cooling systems), agrochemicals (sensitive to moisture, requiring inert gas blanketing). Operators that invest in specialized tankers — with dedicated tank coatings, temperature control, and cleanliness protocols — can command premium freight rates and build strong customer relationships.

-

O2: Digitalization and AI-driven logistics optimization – The industry is accelerating digitalization, with AI-driven logistics platforms optimizing stowage (compatibility algorithms ensuring hazardous cargoes are properly segregated) and voyage planning (weather routing, fuel optimization). Digital platforms also enable real-time tracking, inventory management, and predictive maintenance for vessels and cargo handling equipment. Operators that adopt these technologies can reduce costs, improve safety, and enhance customer service.

-

O3: Sustainability — carbon-neutral fuels and energy-efficient technologies – Sustainability is a key focus: operators are testing carbon-neutral fuels (e.g., methanol-ready tankers, ammonia-ready designs) and adopting energy-efficient cargo handling systems (electric pumps, optimized heating systems, advanced hull coatings). First movers on sustainability can differentiate themselves in the market, attract customers with strong ESG commitments, and benefit from regulatory incentives (e.g., reduced port fees, preferential berthing access).

-

O4: Southeast Asia as a growing hub for chemical imports – Southeast Asia (Vietnam, Thailand, Indonesia, Malaysia, Philippines) is emerging as a major hub for inorganic chemical imports (sulfuric acid, phosphoric acid, caustic soda) to support its rapidly growing manufacturing and construction sectors. Additionally, the region is expanding its petrochemical and specialty chemical production, creating both import and export opportunities for chemical shipping.

-

O5: US strengthening exports of organic intermediates – The US is strengthening its exports of organic intermediates (acetic acid, formaldehyde, ethylene glycol) driven by low-cost natural gas feedstocks (ethylene production) and increasing production capacity. This creates growing export opportunities for chemical tanker operators serving US Gulf-to-Asia and US Gulf-to-Europe routes.

-

O6: Flexible solutions — ISO tank containers for high-value, low-volume shipments – Supply chain diversification is boosting demand for flexible solutions like ISO tank containers (portable tanks that can be moved by sea, road, and rail). Tank containers are particularly suited for high-value, low-volume shipments (pharmaceutical intermediates, specialty chemicals, electronic chemicals) and for routes where dedicated chemical tankers are uneconomic. Operators that offer integrated logistics services (sea + road + rail) or have access to ISO tank container fleets can capture this growing segment.

Industry Structure and Competitive Dynamics

The global Liquid Chemical Seaborne Logistics market is characterized by:

-

Major integrated chemical tanker operators: Stolt-Nielsen (world leader, with a fleet of ~170 vessels), Odfjell (second largest), MOL Chemical Tankers, Hansa Tankers, Team Tankers, Bahri (Saudi-based, rapidly expanding). These operators have large, diversified fleets, long-standing customer relationships, extensive port networks, and sophisticated logistics capabilities.

-

Regional and specialty operators: Inner Mongolia Junzheng Energy and Chemical (China-based, serving domestic and regional routes), Iino Kaiun Kaisha (Japan, specialized in East Asian and Southeast Asian routes), WOMAR (Japan/Singapore, serving Asian routes), MTMM (South Korea). These operators often have lower costs and strong regional networks.

-

New entrants and niche players: Smaller operators specializing in specific cargo types (e.g., electronic chemicals, temperature-controlled cargoes) or specific routes (e.g., US Gulf to East Asia). They compete on flexibility, responsiveness, and specialized expertise.

Key success factors in this market:

-

Vessel quality and fleet composition: Modern, stainless steel, double-hull vessels with advanced cargo handling systems.

-

Regulatory compliance: Robust safety management systems, IBC Code compliance, and strong relationships with regulatory authorities.

-

Customer relationships: Long-term contracts with chemical producers and traders; ability to provide reliable, on-time services.

-

Cost management: Efficient operations, fuel cost management, and effective route planning.

-

Safety record: An impeccable safety record is essential for customer trust and regulatory acceptance.

-

Sustainability credentials: Investment in low-emission technologies and carbon reduction strategies.

-

Digital integration: Use of AI, IoT, and digital platforms for operational optimization and customer engagement.