+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Asia-Pacific Tray Denester Market to Reach $0.14 Billion by 2031, Growing at 5.97% CAGR

Thursday,02 Jul,2026

Tray Denester: Definition and Principles

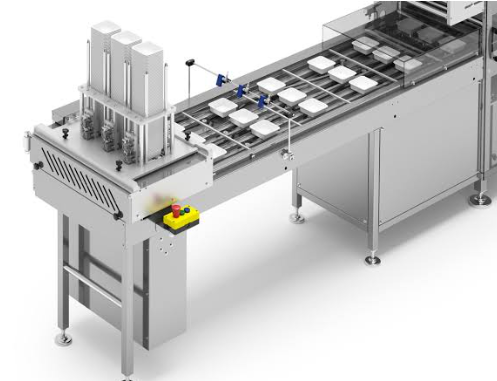

A Tray Denester is a specialized automation device designed to separate and dispense individual trays from a stacked column, enabling efficient and continuous feeding of trays into downstream packaging, filling, or processing lines. It plays a vital role in high-speed production environments, particularly in industries such as food processing, pharmaceuticals, and consumer goods, where hygiene, precision, and throughput are essential. Tray denesters can handle various types of trays—plastic, paperboard, foam, or compostable materials—and are adaptable to different sizes and shapes.

Working principle:

The denesting process involves separating tightly nested trays—which are typically stacked one inside another—and delivering them one at a time to the next station (e.g., filling, sealing, labeling). Common mechanisms include:

-

Vacuum suction: A vacuum gripper lifts the top tray from the stack, overcoming the interlocking friction and surface tension that hold nested trays together.

-

Mechanical separation: Mechanical fingers or pins engage the tray edges to separate and pull individual trays out.

-

Air jet: Compressed air is blown into the gap between trays, breaking the suction effect and allowing separation.

-

Combination of above: Most modern denesters use a combination of vacuum, mechanical grippers, and air jets for reliable separation across diverse tray types.

Key performance characteristics:

-

Speed: Throughput rates can range from 20 to over 200 trays per minute, depending on tray type, size, and machine configuration.

-

Accuracy: Precise alignment and placement for downstream processes.

-

Reliability: Minimal jams or misfeeds, with robust jam detection and recovery systems.

-

Hygiene: Designed with smooth surfaces, minimal crevices, and clean-in-place (CIP) or washdown capability for food and pharmaceutical applications.

-

Flexibility: Quick changeover for different tray sizes and formats (adjustable guides, programmable settings).

-

Durability: Constructed from food-grade stainless steel, aluminum, or other corrosion-resistant materials for long service life.

Common applications:

-

Food processing: Meat, poultry, seafood, bakery, dairy, ready-to-eat meals, produce packaging.

-

Pharmaceuticals: Blister packaging, pill trays, medical device trays.

-

Consumer goods: Cosmetic trays, consumer electronics packaging, retail display trays.

-

E-commerce and logistics: Tray-based sorting and packaging systems.

Tray Denester Market Summary

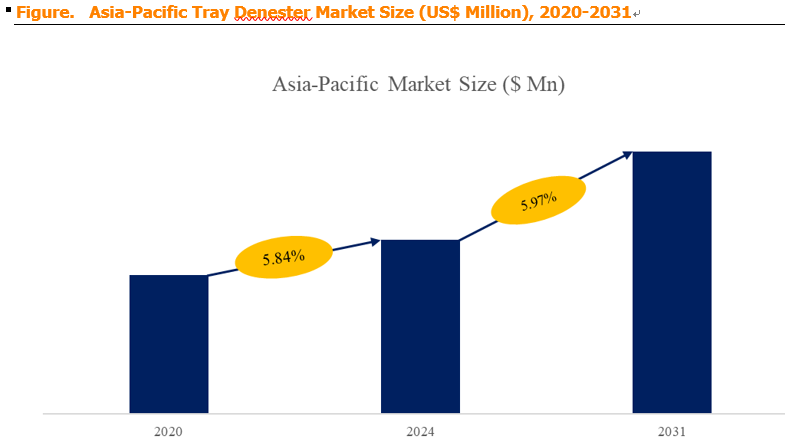

According to a new market research report published by Market Monitor Global, the Asia-Pacific Tray Denester market is projected to reach USD 0.14 billion (approximately $140 million) by 2031, at a compound annual growth rate (CAGR) of 5.97% during the forecast period. The Asia-Pacific region is the fastest-growing and largest market for tray denesters globally, driven by the region's massive food processing industry, rapid expansion of packaged food consumption, labor cost pressures, and increasing automation in manufacturing.

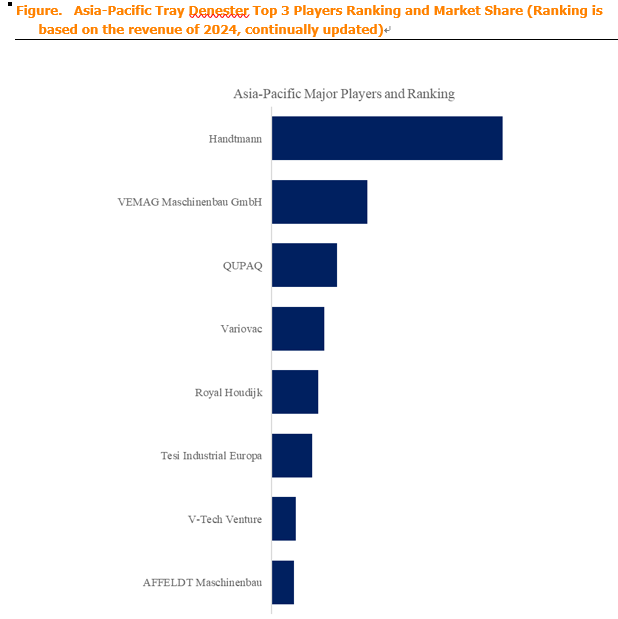

Market Monitor Global's analysis indicates that the Asia-Pacific key manufacturers of Tray Denesters include Handtmann (Germany, with significant Asia-Pacific operations) and VEMAG Maschinenbau GmbH (Germany). In 2024, the Asia-Pacific top three players collectively accounted for approximately 78.1% of total revenue, indicating a highly concentrated market dominated by European manufacturers with strong local presence and partnerships in the Asia-Pacific region. However, there is an emerging presence of local Asian manufacturers (particularly in China, Japan, South Korea, and Southeast Asia) offering lower-cost alternatives for price-sensitive segments.

In terms of product type (by mechanism or configuration), the market is segmented into Vacuum Denesters, Mechanical Denesters, and Combined Denesters. Vacuum-based systems dominate due to their gentle handling, suitability for delicate trays, and reliability across diverse tray types. Electric Denesters (using electric drive systems) are gaining market share over pneumatic models due to improved precision, lower energy consumption, and reduced maintenance requirements.

Regarding application, the Food Industry is the largest segment, accounting for a significant majority of the market. Within food processing, Meat, Poultry, and Seafood packaging is the dominant sub-segment, followed by Bakery, Snacks, and Confectionery; Dairy and Ready-Meals; and Fresh Produce. The Pharmaceutical and Medical segment is a smaller but high-growth segment, driven by strict hygiene and traceability requirements. Consumer Goods (cosmetics, household products, electronics) accounts for the remainder.

Regional dynamics: China is the largest market in the Asia-Pacific region, driven by its massive food processing industry, rapid adoption of automation, and government policies encouraging industrial upgrading (Made in China 2025). Japan and South Korea are mature markets with high automation penetration, focusing on precision, reliability, and advanced features (sensor-based controls, IoT connectivity). Southeast Asia (Thailand, Vietnam, Indonesia, Philippines, Malaysia) is the fastest-growing sub-region, driven by expanding food processing capacity, rising labor costs, and increasing foreign investment in manufacturing. India is an emerging market, with growing demand for packaged food, pharmaceuticals, and consumer goods, though automation adoption is still in early stages in some sectors.

Tray Denester Market Dynamics

Market Drivers:

-

D1: Rising demand for automated food packaging solutions to reduce manual labor – The Asia-Pacific region has historically relied on manual labor for tray handling and feeding. However, labor availability is declining (due to aging populations in Japan, South Korea, and China; labor shortages in Southeast Asia), and labor costs are increasing. Automation of tray handling — starting with denesting — is a cost-effective way to reduce headcount, improve throughput, and maintain consistent quality.

-

D2: Manufacturers seeking to lower operational costs – In addition to labor cost savings, automated denesters reduce waste (damaged trays from manual handling), improve packaging consistency, and reduce rework. Over the lifecycle of the equipment, the total cost of ownership is lower than manual handling, particularly for high-volume production lines.

-

D3: Stringent hygiene regulations driving touchless, automated equipment – Food safety regulations (e.g., China's GB standards, FDA, EU regulations) require rigorous hygiene standards in food processing. Manual handling is a contamination risk; automated denesters reduce human contact with food-contact surfaces. Additionally, denesters designed for washdown (IP65/IP69K) or CIP are preferred for high-hygiene applications.

-

D4: Increased use of flexible packaging — plastic, fiber, and aluminum trays – The shift toward sustainable, lightweight, and functional packaging (e.g., compostable trays, paperboard trays, aluminum trays) creates demand for denesters capable of handling diverse tray materials and geometries. Denester manufacturers are responding with more versatile designs that can handle a wider range of tray formats.

-

D5: Need for continuous, high-speed operations in food lines – High-speed production lines (e.g., poultry processing at 120+ birds per minute, ready-meal lines at 200+ trays per minute) require denesters that can keep pace with upstream and downstream equipment. Any interruption in tray supply causes line stoppages, reducing overall equipment effectiveness (OEE). Reliable, high-speed denesters are essential for maintaining line efficiency.

Market Restraints:

-

R1: Compatibility issues — variability in tray sizes, shapes, and materials – Tray denesters must handle significant variability: different tray sizes (mini trays to family-size trays), shapes (round, rectangular, oval), materials (thin plastic to thick paperboard, compostable materials with variable rigidity), and nesting configurations (some trays nest tightly, others loosely). Inconsistent tray quality (e.g., out-of-spec dimensions, warped trays) can cause jams, misfeeds, and production delays. Changeover between different tray types may require manual adjustments (tools, time) or programmable settings (but still may require mechanical adjustments). Denester manufacturers are addressing this through flexible, self-adjusting designs, but compatibility remains a challenge for end-users with diverse product lines.

-

R2: Mechanical or pneumatic issues causing downtime – Denesters rely on complex mechanical and pneumatic systems (actuators, cylinders, vacuum pumps, valves, sensors). Wear and tear, lubrication issues, component failure, or pneumatic system contamination can cause unscheduled downtime. In high-volume production, even a few minutes of downtime can be costly. Maintenance costs and the need for skilled technicians to diagnose and repair issues are significant operational burdens.

-

R3: Rapid technological shifts — shortened product lifecycles – The pace of innovation in automation and packaging is accelerating. New technologies (electric drives, smart sensors, IoT connectivity, advanced jam detection) may make older models obsolete sooner. End-users may hesitate to invest in new equipment if they anticipate rapid technological change, preferring to lease, rent, or wait for "next-generation" models.

-

R4: Supply chain disruptions — component delays and shortages – Denesters incorporate electronic components (PLCs, sensors, drives, motors), pneumatics (valves, cylinders, fittings), and other components (bearings, belts, seals). Global supply chain disruptions, such as semiconductor shortages, logistics bottlenecks, or regional trade tensions, can delay deliveries of completed denesters or spare parts, impacting production schedules for end-users.

Market Opportunities:

-

O1: Full-line automation integration – Tray denesters are increasingly integrated with filling, sealing, labeling, and packaging systems to enable end-to-end automation. Instead of standalone units, denesters are designed as modular components of fully automated packaging lines, with synchronized controls, shared HMI (human-machine interface), and centralized data collection. Manufacturers offering integrated solutions (denester + filler + sealer + labeler) can capture more value and build stronger customer relationships.

-

O2: Rise of electric denesters over pneumatic models – Electric denesters (using servo motors or linear actuators) offer significant advantages over pneumatic models:

-

Precision: More accurate positioning and control of the denesting process.

-

Energy efficiency: Less energy consumption than compressed air systems (compressed air is energy-intensive to produce).

-

Lower maintenance: Fewer moving parts, no air filtration or lubrication requirements.

-

Quieter operation: Reduced noise levels in the production environment.

-

Easier integration: Direct interfacing with digital control systems (PLC, IoT) without additional pneumatics-to-electronics conversion.

As electric drive technology costs decline and reliability improves, electric denesters are becoming increasingly attractive for both new installations and retrofits.

-

-

O3: Smart and sensor-based control systems – Use of sensors, vision systems, and PLCs is enabling advanced features:

-

Jam detection: Optical or ultrasonic sensors detect tray misalignment or jams, triggering corrective actions (reverse, air blast) or stopping the line before damage occurs.

-

Tray validation: Vision systems confirm correct tray orientation, size, and integrity (no damage, contamination) before loading.

-

Remote diagnostics: Cloud-connected denesters can send alerts, error logs, and performance data to remote service technicians, enabling rapid diagnosis and reduced on-site service visits.

-

Predictive maintenance: Data analysis of machine parameters (cycle count, motor load, valve actuation times) can predict component failures, enabling scheduled maintenance before failure.

-

-

O4: Compact and space-saving models – There is growing demand for compact denesters suitable for smaller production spaces (e.g., smaller food processors, co-packing facilities, mobile production units) or for integration into multi-machine lines where floor space is limited. Compact designs can be lower-cost and easier to install, expanding the addressable market to smaller enterprises.

-

O5: Expansion into pharmaceuticals and medical devices – The pharmaceutical and medical device industry is a high-growth segment for tray denesters, driven by:

-

Strict hygiene requirements: Denesters designed for pharmaceutical use must meet cGMP (current Good Manufacturing Practice) standards, with washdown-capable designs, corrosion-resistant materials, and smooth, crevice-free surfaces.

-

Traceability: Integration with serialization, track-and-trace systems for regulatory compliance (e.g., EU Falsified Medicines Directive).

-

Sensitive products: Tray handling for vials, syringes, cartridges, and medical device components requires gentle handling, precision alignment, and contamination control.

This segment is higher-margin, and manufacturers that specialize in pharmaceutical-grade denesters can command premium pricing.

-

-

O6: Aftermarket services and retrofits – The installed base of tray denesters (both manual and automated) represents a significant aftermarket opportunity:

-

Preventive maintenance contracts: Regular inspection, cleaning, lubrication, and component replacement.

-

Retrofit upgrades: Upgrading older denesters with modern controls (PLC-based, sensor-based), electric drives, or improved jam detection systems.

-

Spare parts supply: Consistent availability of consumables (belts, seals, grippers, valves, sensors) and wear parts.

-

Industry Trends:

-

Full-line automation integration: Tray denesters are increasingly integrated with filling, sealing, and labeling systems to enable end-to-end automation. This integration reduces manual handling, improves efficiency, and enables centralized control and data collection.

-

Rise of electric denesters: Increased adoption of electric drive systems over pneumatic models for improved precision, energy efficiency, lower maintenance, quieter operation, and easier digital integration.

-

Smart and sensor-based control systems: Use of sensors, vision systems, and PLCs for jam detection, tray validation, and remote diagnostics. Predictive maintenance capabilities are being integrated to reduce downtime.

-

Compact and space-saving models: Growth in demand for compact denesters suitable for smaller production spaces or mobile units. Manufacturers are developing smaller footprint designs that maintain performance.

Industry Structure and Competitive Dynamics

The Asia-Pacific Tray Denester market is characterized by:

-

European dominance (Handtmann, VEMAG, others): These German manufacturers have a long history, deep engineering expertise, and strong reputations for quality, reliability, and performance. They dominate the premium segment, with advanced features (electric drives, sensor-based controls, high-speed capability). They have established local presence (subsidiaries, distributors, service centers) across the Asia-Pacific region.

-

Emerging local/regional manufacturers: Particularly in China, Japan, South Korea, and Taiwan, there are local manufacturers offering lower-cost denesters (often simplified designs, reduced feature sets, or leveraging lower-cost components). They are gaining share in price-sensitive segments, particularly in China's domestic market and among smaller enterprises.

-

Chinese manufacturers: Companies like Shandong, Shanghai, and Guangdong-based packaging machinery manufacturers are developing denester products, often as part of larger packaging line solutions. They offer cost-competitive alternatives to European brands, targeting the mid-tier domestic market.

-

Japanese and South Korean manufacturers: Focus on precision, automation, and reliability, with high-performance denesters for advanced applications (pharmaceuticals, high-speed food lines). They compete with European brands in the premium segment.

Key success factors in this market:

-

Product reliability and performance (low jam rates, high throughput, consistent operation).

-

Flexibility and changeover capability (quick, tool-free changeovers for different trays).

-

Hygiene and cleanability (IP ratings, washdown capability, FDA/GRS compliance).

-

Integration capability (compatibility with upstream/downstream equipment, PLC interfaces).

-

After-sales support and service (spare parts availability, maintenance contracts, remote diagnostics).

-

Local presence and responsiveness (fast response to local customer needs, understanding of regional regulations and market requirements).