+1-3236076188

+1-3236076188 sales@marketmonitorglobal.com

sales@marketmonitorglobal.com

Log In

Log In  Log In

Log In Home>News>Global Power Cable and Electrical Equipment Cable Market to Reach $391.97 Billion by 2031, Growing at 4.3% CAGR

Global Power Cable and Electrical Equipment Cable Market to Reach $391.97 Billion by 2031, Growing at 4.3% CAGR

Thursday,02 Jul,2026

Power Cable and Electrical Equipment Cable: Definition and Principles

Wire & Cable are essential components used to transmit electrical power or signals. A wire is a single conductor (usually made of copper or aluminum), while a cable consists of multiple insulated wires bundled together, often with protective sheathing, armor, and outer jackets. They are widely used in electrical systems, telecommunications, and industrial applications. This report focuses specifically on the Power Cable and Electrical Equipment Cable market.

Key product categories:

-

Power Cables (largest segment, 60.5% share): Used for the transmission and distribution of electrical power. Includes:

-

High-voltage (HV) and extra-high-voltage (EHV) cables: For long-distance transmission, often underground or submarine.

-

Medium-voltage (MV) cables: For distribution networks, industrial plants, and large commercial buildings.

-

Low-voltage (LV) cables: For final distribution to end-users, residential, and commercial applications.

-

Underground and submarine cables: For urban distribution, offshore wind farms, and interconnectors.

-

Aerial bundled cables (ABC): Overhead lines with bundled insulated conductors.

-

-

Electrical Equipment Cables: Cables used to connect electrical equipment (motors, generators, transformers, switchgear, control panels, etc.). Includes:

-

Control cables: For signal transmission and control circuits.

-

Instrumentation cables: For precise signal transmission in process industries.

-

Flexible cables: For moving or vibrating equipment.

-

Fire-resistant cables: For safety-critical applications (emergency circuits, fire alarms, evacuation systems).

-

Specialty cables: For extreme environments (high temperature, chemical resistance, nuclear, offshore).

-

Key materials:

-

Conductors: Copper (high conductivity, excellent mechanical properties) and aluminum (lighter, lower cost, used in overhead lines and some power cables). Conductors may be solid or stranded (for flexibility).

-

Insulation: Cross-linked polyethylene (XLPE) — the most common for power cables; PVC (polyvinyl chloride) — used in low-voltage and control cables; EPR (ethylene propylene rubber); paper-oil (traditional, still used in some HV cables); and advanced materials like polypropylene and ethylene-tetrafluoroethylene (ETFE) for high-temperature applications.

-

Sheathing/jacketing: PVC, PE (polyethylene), LSZH (low-smoke zero-halogen), polyurethane, and steel wire armor (SWA) for mechanical protection.

-

Fillers and tapes: For cable roundness, moisture barriers, and fire resistance.

Key performance characteristics:

-

Voltage rating: Determines the cable's maximum operating voltage (low, medium, high, extra-high).

-

Current-carrying capacity (ampacity): Maximum current the cable can safely carry without overheating.

-

Insulation resistance: Ability to prevent current leakage and withstand electrical stress.

-

Mechanical properties: Tensile strength, crush resistance, impact resistance, flexibility.

-

Environmental resistance: UV resistance, moisture resistance, chemical resistance, temperature rating.

-

Fire performance: Flame retardance, smoke emission, toxicity (LSZH cables are increasingly preferred).

-

Service life: Typically 30–50+ years for power cables, depending on material selection and operating conditions.

Power Cable and Electrical Equipment Cable Market Summary

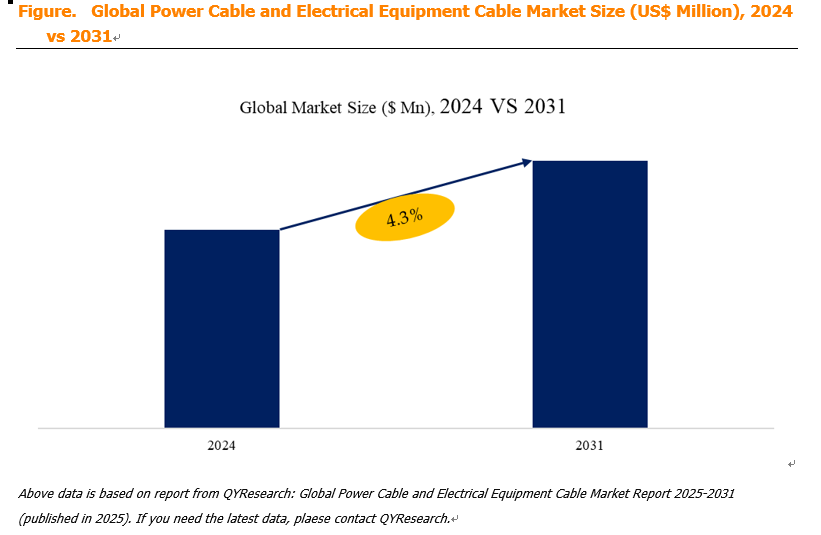

According to a new market research report published by Market Monitor Global, the global Power Cable and Electrical Equipment Cable market is projected to reach USD 391.97 billion by 2031, at a compound annual growth rate (CAGR) of 4.3% during the forecast period. This substantial market size reflects the essential nature of cables in all aspects of electricity generation, transmission, distribution, and consumption, as well as the growing demand for electrification across all sectors.

Market Monitor Global's analysis indicates that the global key manufacturers of Power Cable and Electrical Equipment Cable include Prysmian (Italy), Nexans (France), Baosheng Science and Technology (China), Sumitomo Electric Industries (Japan), Hengtong (China), Jiangsu Shangshang Cable (China), LS Cable & System (South Korea), NKT (Denmark), FAR EAST CABLE (China), and Gold Cup Electric Apparatus (China). In 2024, the global top 10 players collectively accounted for approximately 13.0% of total revenue, indicating a highly fragmented market with numerous local, regional, and specialized players. The cable industry is characterized by large multinational corporations (Prysmian, Nexans, Sumitomo, LS Cable, NKT) that compete globally with extensive product portfolios, R&D capabilities, and global supply chains, alongside a vast number of domestic players (particularly in China and India) that serve local markets with cost-competitive products.

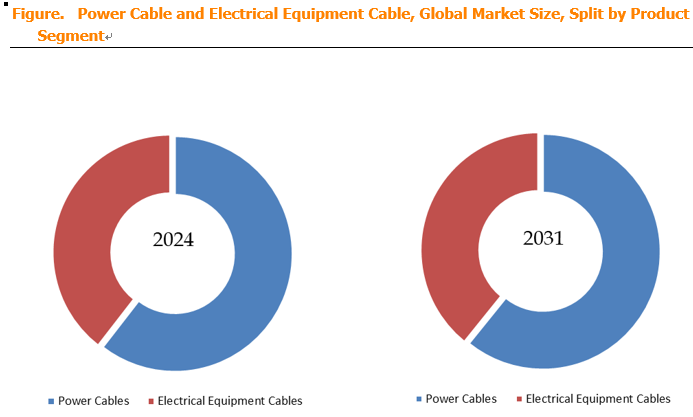

In terms of product type, Power Cables is the largest segment, holding a 60.5% share. This includes high-voltage, medium-voltage, and low-voltage power cables used in transmission and distribution networks, industrial plants, infrastructure projects, and residential/commercial buildings. Electrical Equipment Cables (control cables, instrumentation cables, flexible cables, specialty cables) accounts for the remaining share (approximately 39.5%), driven by industrial automation, manufacturing, renewable energy, and the growing electrification of transportation.

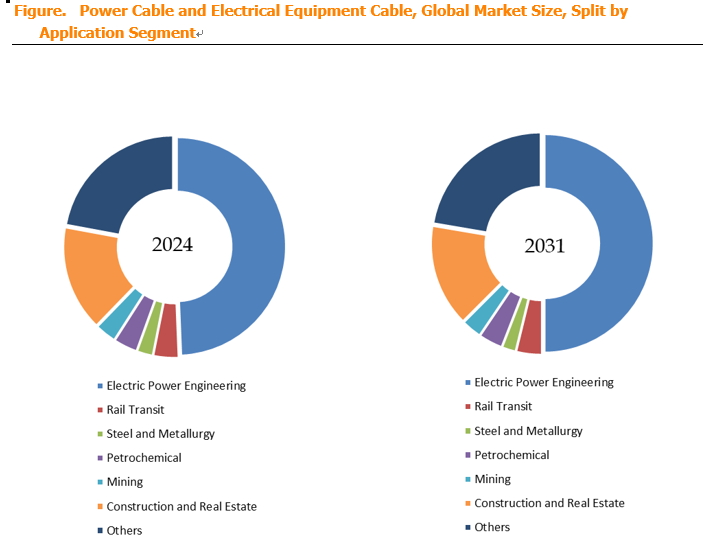

Regarding application, Electric Power Engineering is the largest segment, accounting for 49.4% of the market. This includes power transmission and distribution networks (grid infrastructure, substations, interconnectors), renewable energy projects (offshore wind farms, solar parks), and grid modernization (smart grids, underground cabling). Industrial Manufacturing, Construction and Infrastructure, Transportation (Rail and EV Charging) , Oil & Gas / Energy, and Others account for the remainder.

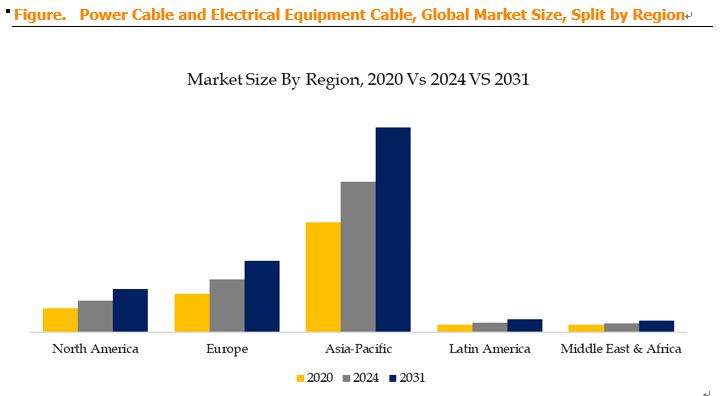

Regional dynamics: Asia-Pacific is the largest and fastest-growing market, driven by China's massive infrastructure investments (grid expansion, renewable energy, urbanization), rapid industrialization in India and Southeast Asia, and the development of smart cities and EV charging networks. Europe is a mature but technologically advanced market, with a strong focus on renewable energy integration (offshore wind in the North Sea, solar in Southern Europe), grid modernization, and high environmental standards (LSZH cables, halogen-free materials). North America is a significant market, driven by aging grid infrastructure replacement, renewable energy investments (particularly in solar and wind), and infrastructure modernization (EV charging, smart grids). The Middle East & Africa and Latin America are smaller but growing markets, driven by infrastructure investment, oil & gas projects, and urbanization.

Power Cable and Electrical Equipment Cable Market Dynamics

Market Drivers:

-

D1: Global surge in electricity demand from urbanization, industrialization, and renewable energy integration – Global electricity consumption is projected to grow by 2-3% annually, driven by increasing electrification of transport (EVs), industry, and buildings, as well as rising population and economic growth in developing countries. The integration of renewable energy sources (solar, wind) into grids requires substantial investment in transmission and distribution infrastructure, including high-voltage and underground cables, connecting remote generation sites to load centers.

-

D2: Government investments in smart grids and EV charging infrastructure – Governments worldwide are investing in smart grid technology (to improve grid reliability, efficiency, and resilience) and EV charging infrastructure. Smart grids require advanced cables with integrated sensors, monitoring capabilities, and communication links. EV charging infrastructure requires high-power DC cables (fast charging), flexible cables for charging stations, and distribution cables for charging hubs.

-

D3: Grid modernization and replacement of aging infrastructure in developed regions – In North America, Europe, and Japan, much of the power grid infrastructure is 50+ years old and reaching end-of-life. Replacement and modernization projects (undergrounding, capacity upgrades, resilience improvements) are driving demand for power cables. The US Bipartisan Infrastructure Law and EU REPowerEU plan include substantial funding for grid upgrades.

-

D4: Electrification of transportation (EVs, rail networks) – The shift from internal combustion engines to electric vehicles is driving demand for charging cables (AC and DC), high-voltage cables for battery systems, and cables for charging station infrastructure. Rail network electrification (high-speed rail, urban transit) also requires specialized cables for overhead lines, signaling, and power distribution.

-

D5: Growth in offshore wind and submarine interconnectors – Offshore wind farms require extensive submarine cable systems (inter-array and export cables) to transmit power from turbines to shore. Cross-border and cross-sea interconnectors (e.g., North Sea Link, NEMO Link) are growing, driven by renewable energy integration and grid resilience. These high-value, high-margin cable segments are a key growth area for leading manufacturers.

-

D6: Rising demand for fire-resistant, low-smoke, and halogen-free cables – Safety regulations and building codes (e.g., EU Construction Products Regulation, US National Electrical Code) increasingly mandate fire-resistant cables (circuit integrity during fire) and low-smoke zero-halogen (LSZH) cables in public buildings, tunnels, and critical infrastructure. These cables are more expensive but offer higher safety performance, driving value growth in the cable market.

Market Restraints:

-

R1: Raw material price volatility (copper, aluminum) – Copper and aluminum are the primary materials for cable conductors. Prices are volatile, influenced by global supply-demand balances, mining disruptions, trade policies (tariffs), and currency fluctuations. This price volatility impacts cable manufacturers' margins and can disrupt project economics (fixed-price contracts for large projects may become unprofitable if material prices rise sharply).

-

R2: Fragmented market with intense price competition – The cable industry is highly fragmented, with many local and regional players competing on price. This leads to thin margins in commodity cable segments, particularly for low-voltage and standard cables. Manufacturers must differentiate through technology, quality, service, and specialized products (submarine cables, EHV, specialty applications) to maintain profitability.

-

R3: Logistics and transportation costs – Cables are heavy, bulky, and require specialized transportation (cable drums, ships for submarine cables). Long-distance shipping adds significant cost and complexity, limiting globalization of the market. Cable manufacturers often locate production near key customers or markets to reduce logistics costs.

-

R4: Technological obsolescence and investment in R&D – The cable industry is undergoing rapid technological change: higher voltage ratings, new materials (XLPE, polypropylene, HTS), smart cables with embedded sensors, and superconducting cables. Manufacturers must continuously invest in R&D to stay competitive. For smaller players, the R&D burden may be too high, limiting their ability to compete in advanced segments.

-

R5: Dependence on large-scale infrastructure projects – Much of the demand for high-value power cables (submarine, EHV, underground) depends on large-scale, long-lead-time infrastructure projects (offshore wind farms, interconnectors, grid upgrades). Project delays (permitting, financing, regulatory approvals) can cause revenue volatility for cable manufacturers.

{HP7M4_LN8.png)

Market Opportunities:

-

O1: High-temperature superconducting (HTS) cables – HTS cables use superconducting materials that have zero electrical resistance at cryogenic temperatures. They can carry much higher currents than conventional cables at lower voltage, making them attractive for urban grids (limited space for new cable corridors) and high-power applications (data centers, heavy industry). HTS cables are still in early commercial stages but represent a disruptive opportunity.

-

O2: IoT-enabled monitoring systems for predictive maintenance – Smart cables with embedded sensors (temperature, partial discharge, strain, moisture) and communication capabilities enable real-time monitoring of cable health, prediction of failures, and optimized maintenance scheduling. This is particularly valuable for underground and submarine cables, where maintenance access is difficult.

-

O3: Eco-friendly materials (recyclable, halogen-free, bio-based) – Stricter environmental regulations (EU RoHS, REACH, China RoHS) and corporate sustainability commitments are driving demand for cables with lower environmental impact. This includes halogen-free flame-retardant compounds, bio-based polymers (from renewable sources), and cables designed for recyclability (mono-material designs). Manufacturers that develop eco-friendly cables can differentiate and capture premium pricing.

-

O4: Automation in manufacturing (Industry 4.0) – Cable manufacturing is being optimized with AI-driven quality control (vision systems for surface defects), predictive maintenance for production equipment, and automated logistics (cable handling, packaging). These technologies reduce waste, improve yield, and reduce labor costs.

-

O5: Replacement of aging grid infrastructure in Asia-Pacific and emerging markets – While developed regions are modernizing, emerging economies (China, India, Southeast Asia, Latin America) are rapidly expanding their grids and replacing aging infrastructure. China's State Grid and Southern Grid continue to invest heavily in UHV and smart grid technologies, while India's "One Nation, One Grid" initiative drives investment in transmission infrastructure.

-

O6: Geopolitical factors — supply chain localization and import substitution – The COVID-19 pandemic and geopolitical tensions (US-China, Russia-Ukraine, EU-China) have highlighted supply chain vulnerabilities. Governments are encouraging local production of critical infrastructure components, including cables. This provides opportunities for domestic cable manufacturers (e.g., in the US, EU, India) and may limit imports, altering global trade patterns.

-

O7: Recycling and alternative conductive materials – Copper and aluminum prices are high and volatile. There is growing interest in:

-

Recycling: Recovering copper and aluminum from decommissioned cables and scrap to reduce raw material costs.

-

Alternative conductors: Aluminum alloys (AA-8000 series) with improved mechanical properties; carbon nanotube composites (still experimental but potentially high conductivity).

-

Superconducting materials: As noted above, but also simpler technologies like advanced alloy formulations.

Manufacturers that invest in recycling and alternative conductor technologies can reduce material costs and improve sustainability credentials.

-

Industry Structure and Competitive Dynamics

The global Power Cable and Electrical Equipment Cable market is characterized by:

-

Global leaders (Prysmian, Nexans, Sumitomo, LS Cable, NKT): These companies have extensive product portfolios, strong R&D capabilities, global manufacturing footprints, and long track records in high-value projects (submarine, EHV, offshore wind). They dominate the premium and technology-intensive segments.

-

Major Chinese manufacturers (Baosheng, Hengtong, Jiangsu Shangshang, FAR EAST CABLE, Gold Cup): These companies benefit from the massive domestic market, government support, cost advantages (labor, raw materials), and aggressive expansion into international markets. They are becoming increasingly competitive in technology and quality, challenging European and Japanese incumbents.

-

Regional and specialty players: Numerous local and regional manufacturers (including in India, Southeast Asia, Latin America, Eastern Europe) serving domestic markets with standard cables. They compete on price and customer relationships.

-

Niche players: Companies specializing in specific segments (e.g., submarine cables, high-temperature cables, fire-resistant cables, instrumentation cables) with deep application expertise.

Key success factors in this market:

-

Technology and innovation: R&D investment in new materials, higher voltages, smart cables, and specialty applications.

-

Quality and reliability: Cable failures can have severe safety and economic consequences; customers value proven, reliable products.

-

Project execution capability: Ability to manage large-scale, complex projects (design, manufacturing, installation, commissioning).

-

Global supply chain and logistics: Access to raw materials, manufacturing capacity, and logistics for international delivery.

-

Customer relationships and service: Strong relationships with utilities, OEMs, industrial customers, and government agencies.

-

Cost competitiveness: Efficient manufacturing, material sourcing, and supply chain management.

-

Sustainability credentials: Eco-friendly materials, recycling, and low-carbon manufacturing processes.